What is the minimum credit score I need to qualify for a Kentucky mortgage currently?

Question:

What is the current minimum credit scores needed to qualify for a Kentucky mortgage Loan?

Answer:

The minimum credit score needed to qualify for a Kentucky mortgage depends on the type of loan program you are looking to obtain, this could be the reason that you have received conflicting answers.

The most common types of mortgage are Conventional, FHA, USDA, VA, and KHC mortgage loans in Kentucky. I’ll explain each briefly below and the minimum credit score needed to qualify for each loan program. Keep in mind these are continuously changing and can vary by lender do to credit overlays.

Kentucky Conventional or Fannie Mae

Conventional loans make up the majority of mortgages in the US. They are also known as conforming loans, because they conform to specific guidelines set by Fannie Mae and Freddie Mac.

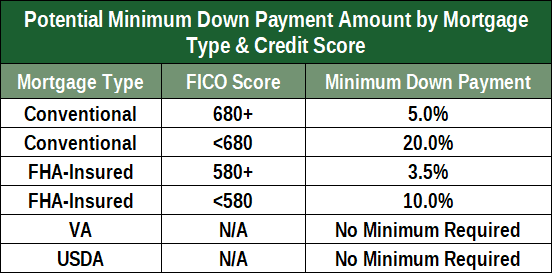

- Minimum Credit Score is 620

- What Are the Conforming Loan Limits for 2024?

Property Type Minimum Conforming Loan Limit Maximum Conforming Loan Limit

One-unit $766,550 $1,149,825

Two-unit $981,500 $1,472,250

Three-unit $1,186,350 $1,779,525

Four-unit $1,474,400 $2,211,600 - You can use a conventional loan to buy a primary residence, second home, or rental property

- Conventional loans are available in fixed rates, adjustable rates (ARMs), and offer many loan terms usually from 10 to 30 years

- Down payments as low as 3% and 5% depending on Home Ready or straight conventional loan.

- No monthly mortgage insurance with a down payment of at least 20%

- Max Debt to Income Ratio of 50%

KENTUCKY FHA MORTGAGE

An FHA loan is a mortgage issued by federally qualified lenders and insured by the Federal Housing Administration (FHA). FHA loans are designed for low-to-moderate income borrowers who are unable to make a large down payment.

- Minimum Credit Score is 500 with at least 10% down

- Minimum Credit Score is 580 if you put less than 10% down

- The maximum loan amount varies by Geographical Area, for 2024 is $498,257

- Upfront and Monthly Mortgage Insurance is required regardless of the Loan to Value

- FHA Loans are only available for financing primary residences

- Maximum Debt to Income Ratio of 50% (unless mitigating factors justify allowing a higher DTI) up to 57% in some instances with strong compensating factors.

KENTUCKY USDA RURAL HOUSING LOAN

-

- 100% Financing

- Cities and towns located outside metro areas-see link (https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do?pageAction=sfp

- Do NOT have to be a Kentucky First Time Home Buyer

- No Down Payment

- 30 year low fixed rate loans

- No Prepayment Penalty

- Great Low FIXED Interest Rates

- No max loan limits, just income limits

- Possible to Roll Closing Costs into Loan if Appraises Higher

- No Cash Reserves Required

- UNLIMITED Seller Contribution toward Closing Costs

- 100% Gifted Closing Costs allowed

- Primary Residents only (no rentals/investment properties)

- Debt to income ratios no more than 45% with GUS approval and 29 and 41% with a manual underwrite.

- Only Need a 580 Credit Score to Apply*** Most USDA loans need a 620 or score higher to get approved through their automated underwriting system called GUS. 640 usually required for an automated approval upfront.

- No bankruptcies (Chapter 7) last 3 years and no foreclosure last 3 years. If Chapter 13 bankruptcy possible to go on after 1 year

-

KENTUCKY VA Mortgage

- 100% Financing Available up to qualifying income and entitlement

- Must be eligible veteran with Certificate of Eligibility. We can help get this for veterans or active duty personnel.

- No Down Payment Required

- Seller Can Pay ALL Your Closing Costs

- No Monthly Mortgage Insurance

- Minimum 580 typically Credit Score to Apply–VA does not have a minimum credit score but lenders will create credit overlays to protect their interest.

- Active Duty, Reserves, National Guard, & Retired Veterans Can Apply

- No bankruptcies or foreclosures in last 2 years and a clear CAVIRS

- Debt to income ratios vary, but usually 55% back-end ratio with a fico score over 620 will get it done on qualifying income and if it is a manual underwrite, 29% and 41% respectively

- Can use your VA loan guaranty more than once, and in some cases, can have two existing VA loans out at they same time. Call or email for more info on this scenario.

- Cost of VA loan appraisal in Kentucky now costs a minimum $605 with a termite report needed on all purchase and refinance transactions unless a condo.

- 2 year work history needed on VA loans unless you can show a legitimate excuse, ie. off work due to injury, schooling, education etc.

- You cannot use your GI Bill for income qualifying for the mortgage payment.

KENTUCKY HOUSING DOWN PAYMENT ASSISTANCE 100 FINANCING

Down Payment: There are still housing programs that exist for Kentucky home buyers whereas you can purchase a home with no down payment. You will need a 620 mid credit score to purchase a home using the KHC loan programs for their no down payment credit requirements.

How the Down Payment Assistance Program (DAP) Works

Down payment assistance loans are available up to $10,000 and is paid back over a period of ten years at a current rate of 3.75%.

Regular DAP

- Purchase price up to $481,176 with Secondary Market or Mortgage Revenue Bond (MRB) income limits.

- Assistance in the form of a loan up to $10,000 in $100 increments.

- Repayable over a 10-year term at 3.75 percent.

- Available to all KHC first-mortgage loan recipients

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people