A Kentucky Mortgage Loan Officer that has closed over 600 home loans specializing in Kentucky First Time Homebuyer Loans to include the following FHA, VA, USDA, Rural Housing, Down Payment Assistance Loan from Kentucky Housing Corp or KHC and the Fannie Mae Home Path HUD $100 Down Mortgage Program in Kentucky. Call/Text 502-905-3708 with your mortgage questions or email kentuckyloan@gmail.com I try to respond to all requests within minutes during regular business hours. NMLS# 57916 Joel Lobb Loan Originator, American Mortgage Solutions NMLS ID. 1364 Equal Housing Lender

Acceptable Income and Job History for a Mortgage Loan Approval in Kentucky

Mortgage Underwriters must follow both DU and agency guidelines when it comes to documenting and calculating qualifying income for a loan transaction. Income guidelines may vary slightly depending on the loan program and the borrower’s employment profile. Below are some general tips for W2 income.

Documentation that may be required

Paystub with year to date gross earnings

At least 1 year’s W2

Verbal or full VOE

Base Pay:

Salaried and fixed hourly income is calculated by averaging the gross year to date income

Variable hourly income is calculated by averaging 12 month history

Commission and tip income is calculated by averaging over 24 months

No transcripts are required for salaried, hourly, or less than 25% commission W2 income borrowers

Unreimbursed expenses do not have to be deducted from the gross pay for salaried, hourly, or less than 25% commission W2 borrowers

Overtime, and Bonus Income:

Overtime and Bonus can be used as effective income as long as it’s been received for 2 years and is reasonably likely to continue

Periods of less than 2 years may be considered as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

Overtime and Bonus income must be documented by a full VOE

Declining overtime and bonus income cannot be used for qualifying income

Part Time Income:

FHA loans requires a 2 year history of working multiple jobs

Fannie Mae or Conventional loans will allow less than 2 years as long as it’s been consistently earned over a period of at least 12 months and there are positive factors to offset the shorter history of receipt per underwriter discretion

How to get approved for a Kentucky FHA, VA, USDA and Fannie Mae Mortgage loan with Variable Income

Variable INCOME if your borrower is not hourly at 40 hours a week or salary do you fall within VARIABLE INCOME?? Yup we all dislike that is calculated by an averaging method..

Examples of income of this type include income from hourly workers with fluctuating hours, or income that includes commissions, bonuses, or overtime.

History of Receipt: Two or more years of receipt of a particular type of variable income is recommended; however, variable income that has been received for 12 to 24 months may be considered as acceptable income, as long as the borrower’s loan application demonstrates that there are positive factors that reasonably offset the shorter income history.

Frequency of Payment: us as a lender must determine the frequency of the payment Examples:

If a borrower is paid an annual bonus on March 31st of each year, the amount of the March bonus should be divided by 12 to obtain an accurate calculation of the current monthly bonus amount.

Note that dividing the bonus received on March 31st by three months produces a much higher, INACCURATE monthly average.

If a borrower is paid overtime on a biweekly basis, the most recent paystub must be analyzed to determine that both the current overtime earnings for the period and the year-to-date overtime earnings are consistent and, if not, why.

There are legitimate reasons why these amounts may be inconsistent yet still eligible for use as qualifying income. For example, borrowers may have overtime income that is cyclical (transportation employees who operate snow plows in winter, package delivery service workers who work longer hours through the holidays).

We must investigate the difference between current period overtime and year-to-date earnings and document the analysis before using the income amount in the trending analysis.

Income Trending: After the monthly year-to-date income amount is calculated, it must be compared to prior years’ earnings using the borrower’s W-2’s or signed federal income tax returns (or a standard Verification of Employment completed by the employer or third-party employment verification vendor).

If the trend in the amount of income is stable or increasing, the income amount should be averaged.

If the trend was declining, but has since stabilized and there is no reason to believe that the borrower will not continue to be employed at the current level, the current, lower amount of variable income must be used.

If the trend is declining, the income may not be stable.

Additional analysis must be conducted to determine if any variable income should be used, but in no instance may it be averaged over the period when the declination occurred.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

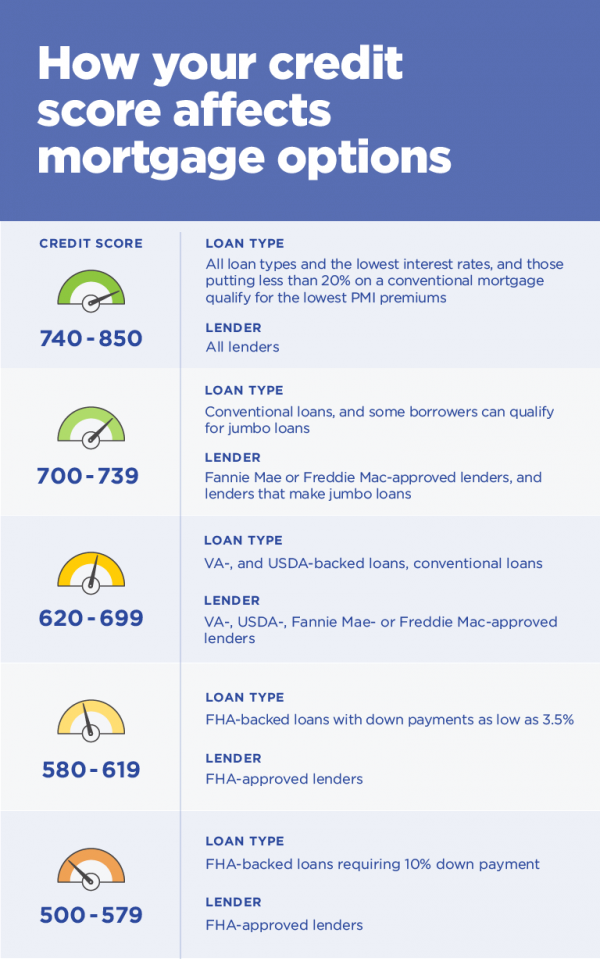

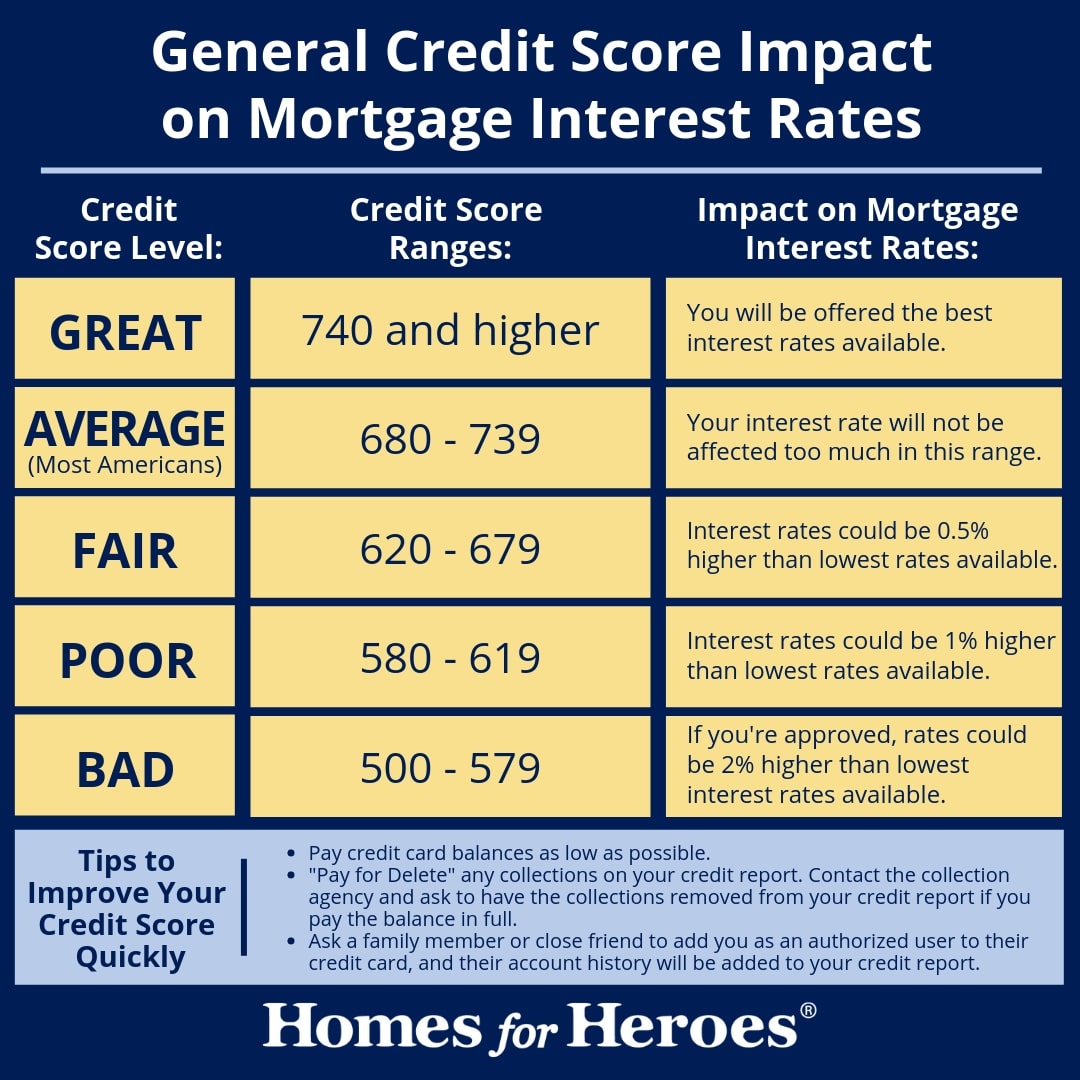

Credit Score Requirements for FHA, VA, USDA and Conventional Loans in Kentucky

Below I have spelled out some info that will help you out when you look at your credit scores and what affects them and what you can do to help your credit scores in order to prepare for a mortgage loan approval when it comes to your credit scores.

Opting out will help a credit score. No it won’t. The bureaus don’t know if someone has opted out or not and it’s not factored into the credit scores. If someone’s score improves after they have opted out it’s because something else has changed on the report but not because they opted out.

Paying off old delinquencies will remove them from your credit report. No a collection account or an account with late payments will stay on a credit report for 7 years. That being said, the credit bureaus will occasionally go in and remove old collections that have not reported for a while. But that’s at their discretion. Just because you paid if off doesn’t mean it will be removed. Also paying off an older collection with then brings the reporting date current which could actually hurt the credit scores.

Opening new accounts will help your credit score. This will help only if the borrower has no established credit yet. Once you have several accounts, opening new ones will actually have a negative affect on a credit score until substantial history is accumulated on the account.

Paying off all your revolving balances is a good thing! Actually no it’s not. The credit bureaus models like to see at least one revolving balance, even if it’s small. Having no revolving balances can actually have a negative impact on a credit score. So always keeping one account with a small balance is a very good idea.

Your credit is affected by how much money you have in your savings or checking accounts. Neither of these are factored into a credit score.

Closing old accounts will help a credit score. The credit scoring models like to see several open accounts that have zero balances and are not used often. When an account is closed you lose that history. If it’s an account you’ve had for a long time and has no late payments, closing it can actual hurt the credit score. Having several open accounts, even if they are not used much, makes it look like a person has good financial responsibility.

When I check my own credit score it’s the same one used by lenders. Unfortunately no it’s not. A person actually has 69+ different credit scores. The ones that lenders use are completely different than what a borrower sees when they get their own scores. Those are personal scores and are not used by any industry for any reason.

Checking my own credit report will hurt my score. When a consumer checks their own credit report it’s a “soft” inquiry and will not impact the scores. Only “hard” inquiries done by creditors when a consumer applies for a loan or credit card will possibly have a negative affect on a credit score.

It’s possible to avoid paying for your credit score or at least an estimate. Here is a list of all of the well-known ways to get a FICO score or score estimate for free:

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

—

Score Requirement on Kentucky FHA Loans for people with bad credit Lowers Minimum Credit Score Requirement on Kentucky FHA Loans

Kentucky FHA Home loan programs for people with bad credit

FHA loans are designed to make housing more affordable with lower down payment requirements than conventional loans on purchases and less home equity requirements on refinances. Less stringent qualification guidelines and the security of a government-insured loan makes FHA a popular choice for consumers.

Kentucky FHA Loans with 580 Credit scores and – Low Down Payment – 3.5% which can be gifted from relatives or borrowed off one’s retirement account. If your scores is between 500-579, 10% down needed for home loan and subject to underwriting approval.

Which Credit Score is used for a Kentucky Mortgage Loan Approval? Credit score used for a Kentucky Mortgage Loan Approval for FHA, VA, USDA Rural Housing, KHC Down payment assistance FAnnie MaeFICO Scores used for mortgages

Does FHA Restrict down payment requirements on Identity of Interest Transactions?

The 85 percent maximum LTV restriction does not apply for Kentucky FHA Loans in regards to FHA Identity-of-Interest transactions under the following circumstances:

👇👇👇

FAMILY MEMBER TRANSACTIONS• the principal residence of another family member; or a property owned by another family member in which the borrower has been a tenant for at least six months immediately predating the sales contract. A lease or other written evidence to verify occupancy is required.

BUILDER’S EMPLOYEE PURCHASE• An employee of a builder, who is not a family member, purchases one of the builder’s new houses or models as a principal residence.

CORPORATE TRANSFER • A corporation transfers an employee to another location, purchases the employee’s house, and sells the house to another employee.

TENANT PURCHASE• the current tenant purchases the property where the tenant has rented the property for at least…

When you get a mortgage, you’re signing a million sheets of paper and agreeing to pay a lot of things that you may not understand at the time. Closing costs, down payments, inspections, real estate agent fees, home insurance, escrow, and so on and so forth. One of the numbers that may have gotten rolled into that list is mortgage insurance premiums.

If you got an FHA loan, you’re almost certainly paying FHA mortgage insurance premiums. Read on to learn more about what these are, how much you might be paying each month, and how you can get out from under them.

Examples of income of this type include income from hourly workers with fluctuating hours, or income that includes commissions, bonuses, or overtime.

Examples of income of this type include income from hourly workers with fluctuating hours, or income that includes commissions, bonuses, or overtime.