A Kentucky Mortgage Loan Officer that has closed over 600 home loans specializing in Kentucky First Time Homebuyer Loans to include the following FHA, VA, USDA, Rural Housing, Down Payment Assistance Loan from Kentucky Housing Corp or KHC and the Fannie Mae Home Path HUD $100 Down Mortgage Program in Kentucky. Call/Text 502-905-3708 with your mortgage questions or email kentuckyloan@gmail.com I try to respond to all requests within minutes during regular business hours. NMLS# 57916 Joel Lobb Loan Originator, American Mortgage Solutions NMLS ID. 1364 Equal Housing Lender

If you’re planning to buy a home in Kentucky in 2024, here are some essential steps to consider:

1. Focus on improving your credit score to qualify for a mortgage with a low interest rate.

2. Manage your debt-to-income ratio by repaying existing debt, increasing your income, or both.

3. Ensure timely payments on all accounts to maintain a good credit score.

4. Get pre-approved for a mortgage before searching for a home to know your affordability.

5. Keep credit card utilization below 30% and seek down payment assistance programs if needed.

Here are action steps you can take right now to buy a home in Kentucky in 2024

1. Focus on your credit score

FICO credit scores are among the most frequently used credit scores, and range from 350-800 (the higher, the better). A consumer with a credit score of 750 or higher is considered to have excellent credit, while a consumer with a credit score below 620 is considered to have poor credit.

To qualify for a mortgage and get a low mortgage rate, your credit score matters.

Each credit bureau collects information on your credit history and develops a credit score that lenders use to assess your riskiness as a borrower. If you find an error, you should report it to the credit bureau immediately so that it can be corrected.

2. Manage your debt-to-income ratio

Many lenders evaluate your debt-to-income ratio when making credit decisions, which could impact the interest rate you receive.

A debt-to-income ratio is your monthly debt payments as a percentage of your monthly income. Lenders focus on this ratio to determine whether you have enough excess cash to cover your living expenses plus your debt obligations.

Since a debt-to-income ratio has two components (debt and income), the best way to lower your debt-to-income ratio is to:

repay existing debt;

earn more income; or

do both

3. Pay attention to your payments

Simply put, lenders want to lend to financially responsible borrowers.

Your payment history is one of the largest components of your credit score. To ensure on-time payments, set up autopay for all your accounts so the funds are directly debited each month.

FICO scores are weighted more heavily by recent payments so your future matters more than your past.

In particular, make sure to:

Pay off the balance if you have a delinquent payment

Don’t skip any payments

Make all payments on time

4. Get pre-approved for a mortgage before you start shopping for a home loan.

Too many people find their home and then get a mortgage.

Switch it.

Get pre-approved with a lender first. Then, you’ll know how much home you can afford.

To get pre-approved, lenders will look at your income, assets, credit profile and employment, among other documents.

5. Keep credit utilization low on your credit cards

Lenders also evaluate your credit card utilization, or your monthly credit card spending as a percentage of your credit limit.

Ideally, your credit utilization should be less than 30%. If you can keep it less than 10%, even better.

For example, if you have a $10,000 credit limit on your credit card and spent $3,000 this month, your credit utilization is 30%.

Here are some ways to manage your credit card utilization:

set up automatic balance alerts to monitor credit utilization

ask your lender to raise your credit limit (this may involve a hard credit pull so check with your lender first)

pay off your balance multiple times a month to reduce your credit utilization

6. Look for down payment assistance in Kentucky

There are various types of down payment assistance, even if you have student loans.

Here are a few:

FHA loans – federal loan through the Federal Housing Authority

USDA loans – zero down mortgages for rural and suburban homeowners

VA loans – if military service

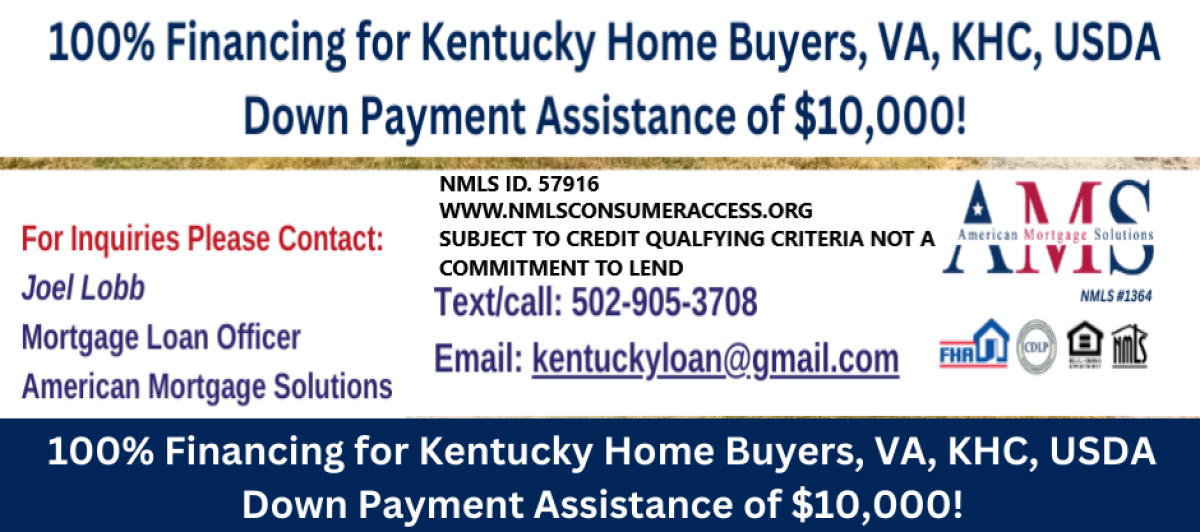

Kentucky Housing Down Payment Assistance of $10,000

There are federal, state and local assistance programs as well so be on the look out.

If you want a personalized answer for your unique situation call, text, or email me or visit my website below:

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

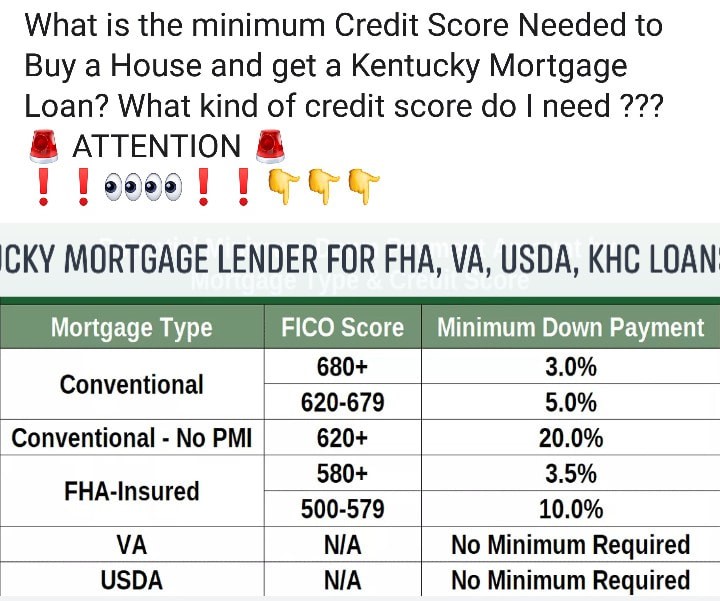

What is the minimum credit score I need to qualify for a Kentucky mortgage currently?

Question:

What is the current minimum credit scores needed to qualify for a Kentucky mortgage Loan?

Answer:

The minimum credit score needed to qualify for a Kentucky mortgage depends on the type of loan program you are looking to obtain, this could be the reason that you have received conflicting answers.

The most common types of mortgage are Conventional, FHA, USDA, VA, and KHC mortgage loans in Kentucky. I’ll explain each briefly below and the minimum credit score needed to qualify for each loan program. Keep in mind these are continuously changing and can vary by lender do to credit overlays.

Kentucky Conventional or Fannie Mae

Conventional loans make up the majority of mortgages in the US. They are also known as conforming loans, because they conform to specific guidelines set by Fannie Mae and Freddie Mac.

Minimum Credit Score is 620

What Are the Conforming Loan Limits for 2024?

Property Type Minimum Conforming Loan Limit Maximum Conforming Loan Limit

One-unit $766,550 $1,149,825

Two-unit $981,500 $1,472,250

Three-unit $1,186,350 $1,779,525

Four-unit $1,474,400 $2,211,600

You can use a conventional loan to buy a primary residence, second home, or rental property

Conventional loans are available in fixed rates, adjustable rates (ARMs), and offer many loan terms usually from 10 to 30 years

Down payments as low as 3% and 5% depending on Home Ready or straight conventional loan.

No monthly mortgage insurance with a down payment of at least 20%

Max Debt to Income Ratio of 50%

KENTUCKY FHA MORTGAGE

An FHA loan is a mortgage issued by federally qualified lenders and insured by the Federal Housing Administration (FHA). FHA loans are designed for low-to-moderate income borrowers who are unable to make a large down payment.

Minimum Credit Score is 500 with at least 10% down

Minimum Credit Score is 580 if you put less than 10% down

The maximum loan amount varies by Geographical Area, for 2024 is $498,257

Upfront and Monthly Mortgage Insurance is required regardless of the Loan to Value

FHA Loans are only available for financing primary residences

Maximum Debt to Income Ratio of 50% (unless mitigating factors justify allowing a higher DTI) up to 57% in some instances with strong compensating factors.

Primary Residents only (no rentals/investment properties)

Debt to income ratios no more than 45% with GUS approval and 29 and 41% with a manual underwrite.

Only Need a 580 Credit Score to Apply*** Most USDA loans need a 620 or score higher to get approved through their automated underwriting system called GUS. 640 usually required for an automated approval upfront.

No bankruptcies (Chapter 7) last 3 years and no foreclosure last 3 years. If Chapter 13 bankruptcy possible to go on after 1 year

KENTUCKY VA Mortgage

100% Financing Available up to qualifying income and entitlement

Must be eligible veteran with Certificate of Eligibility. We can help get this for veterans or active duty personnel.

No Down Payment Required

Seller Can Pay ALL Your Closing Costs

No Monthly Mortgage Insurance

Minimum 580 typically Credit Score to Apply–VA does not have a minimum credit score but lenders will create credit overlays to protect their interest.

Active Duty, Reserves, National Guard, & Retired Veterans Can Apply

No bankruptcies or foreclosures in last 2 years and a clear CAVIRS

Debt to income ratios vary, but usually 55% back-end ratio with a fico score over 620 will get it done on qualifying income and if it is a manual underwrite, 29% and 41% respectively

Can use your VA loan guaranty more than once, and in some cases, can have two existing VA loans out at they same time. Call or email for more info on this scenario.

Cost of VA loan appraisal in Kentucky now costs a minimum $605 with a termite report needed on all purchase and refinance transactions unless a condo.

2 year work history needed on VA loans unless you can show a legitimate excuse, ie. off work due to injury, schooling, education etc.

You cannot use your GI Bill for income qualifying for the mortgage payment.

KENTUCKY HOUSING DOWN PAYMENT ASSISTANCE 100 FINANCING

Down Payment: There are still housing programs that exist for Kentucky home buyers whereas you can purchase a home with no down payment. You will need a 620 mid credit score to purchase a home using the KHC loan programs for their no down payment credit requirements.

How the Down Payment Assistance Program (DAP) Works

Down payment assistance loans are available up to $10,000 and is paid back over a period of ten years at a current rate of 3.75%.

Assistance in the form of a loan up to $10,000 in $100 increments.

Repayable over a 10-year term at 3.75 percent.

Available to all KHC first-mortgage loan recipients

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people

Summary:

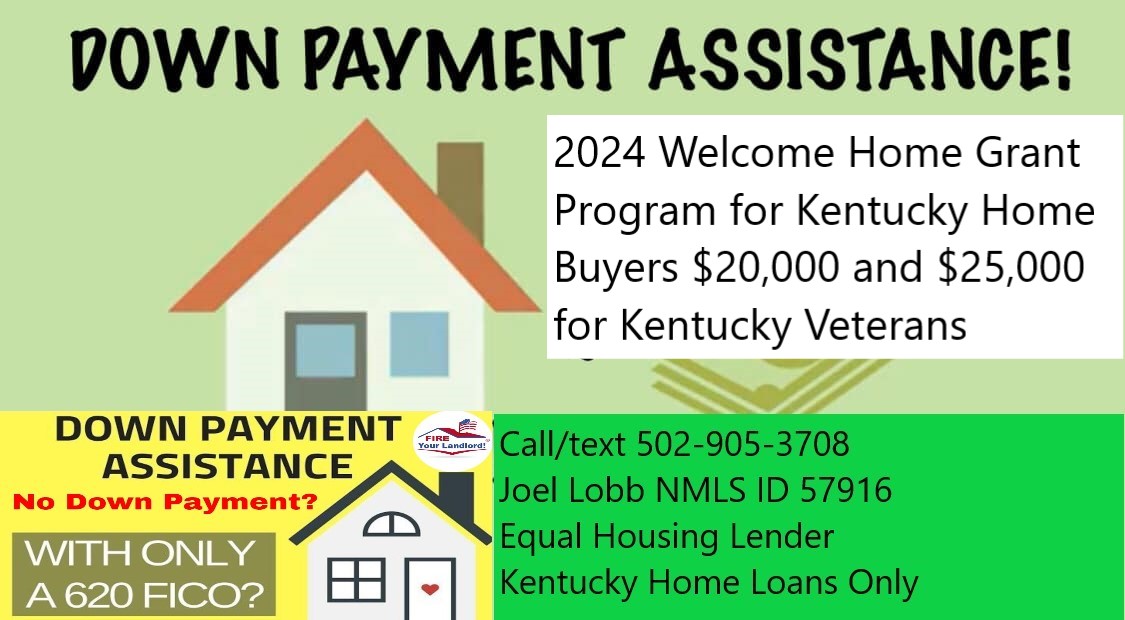

The Welcome Home Program in Kentucky offers grants up to $25,000 for military homebuyers and up to $20,000 for other eligible buyers to assist with down payment and closing costs. Eligible homebuyers must meet income criteria and other guidelines. Properties eligible for the grant must be the buyer’s primary residence and have a legally enforceable retention mechanism. Prospective homebuyers should contact an FHLB Cincinnati Member financial institution for more program information and eligibility details. Various other programs and grants are also available for first-time homebuyers in Kentucky. For further information, contact a Kentucky Mortgage Lender.

Kentucky Down payment assistance loans are available up to $20,000 for Mortgage with Welcome Home Grant 2024

Welcome Home Program Grant Program for Kentucky Home buyers in 2024

Information for Kentucky Homebuyers Welcome Home Program Grant Program for Kentucky Home buyers in 2024

The Federal Home Loan Bank of Cincinnati (FHLB Cincinnati) offers grants of up to $25,000 for honorably discharged veterans, surviving spouses of military personnel, and active duty military homebuyers and up to $20,000 for all other homebuyers to assist with down payment and closing costs for income eligible homebuyers through the Welcome Home Program (WHP).

Kentucky Homebuyers must apply and qualify for a mortgage loan with one of our Member financial institutions to utilize the grant.

Who are Eligible Homebuyers in Kentucky for the Welcome Grant?

A Kentucky homebuyer would be eligible for the Welcome Home grant if all of the following guidelines are met:

The total income for all occupants who will reside in the home is at or below 80 percent of the Mortgage Revenue Bond (MRB) limit for the county and state where the property is located; A fully executed (signed by buyer and seller) purchase contract on an eligible property is in hand; The homebuyer has at least $500 of their own funds to contribute towards down payment and/or closing costs; and, If a first-time homebuyer (typically anyone who has not owned a home in the last three years), a satisfactory homebuyer counseling course is completed prior to the loan closing. Note: Applicants do not have to be first-time homebuyers.

What is an Eligible Property?

A property would be eligible if all of the following guidelines are met:

The property will be the homebuyer’s primary residence; The property is a single family, townhome, condominium, duplex, multi-unit (up to four family units) or a qualified manufactured home. (Manufactured homes may be eligible if they are taxed as real estate and affixed to a permanent foundation); and, The property is subject to a legally enforceable five-year retention mechanism, included in the Deed or as a Declaration of Restrictive Covenants to the Deed, requiring the FHLB Cincinnati be given notice of any refinancing, sale, foreclosure, deed in-lieu of foreclosure, or change in ownership during the five year retention period.

How Do I Apply?

For more program information, homebuyers should contact a FHLB Cincinnati Member financial institution.

HUD HOME Program — Kentucky contacts: HUD provides grant money to communities designated as participating jurisdictions for assisting home buyers, rental assistance, and other housing initiatives

Habitat for Humanity: Through volunteer labor and donations of money and materials, Habitat builds and rehabilitates simple, decent houses with the help of the homeowner (partner) families

Federal Home Loan Bank of Cincinnati: Serves Kentucky residents by offering various home buying assistance programs, including Welcome Home grants. For more information, you may call 1 (888) 345-2246

2024 Welcome Home Grant Program for Kentucky Home Buyers $20,000

Kentucky First Time Home Buyer Common Questions and Answers:

∘ WHAT KIND OF CREDIT SCORE DO I NEED TO QUALIFY FOR DIFFERENT FIRST TIME HOME BUYER LOANS IN KENTUCKY?

Answer. Most lenders will wants a middle credit score of 580 to 620 for KY First Time Home Buyers looking to go no money down. The two most used no money down home loans in Kentucky being USDA Rural Housing and KHC with their down payment assistance will want a 620 middle score on their programs.

If you have access to 3.5% down payment, you can go FHA and secure a 30 year fixed rate mortgage with some lenders with a 580 credit score. Even though FHA on paper says they will go down to 500 credit score with at least 10% down payment, you will find it hard to get the loan approved because lenders will create overlays to protect their interest and maintain a good standing with FHA and HUD.

Another popular no money down loan is VA. Most VA lenders will want a 580 middle credit score but like FHA, VA on paper says they will go down to a 500 score, but good luck finding a lender for that scenario.

A lot of times if your scores are in the high 500’s or low 600’s range, we can do a rapid rescore and get your scores improved within 30 days.

∘ DOES IT COSTS ANYTHING TO GET PRE-APPROVED FOR A MORTGAGE LOAN?

Answer: Most lenders will not charge you a fee to get pre-approved, but some lenders may want you to pay for the credit report fee upfront. Typically costs for a tri-merge credit report for a single borrower runs about $50 or less. Maybe higher if more borrowers are included on the loan application.

∘ HOW LONG DOES IT TAKE TO GET APPROVED FOR A MORTGAGE LOAN IN KENTUCKY?

Answer: Typically if you have all your income and asset documents together and submit to the lender, they typically can get you a pre-approval through the Automated Underwriting Systems within 24 hours.

They will review credit, income and assets and run it through the different AUS (Automated Underwriting Systems) for the template for your loan pre-approval. Fannie Mae uses DU, or Desktop Underwriting, FHA and VA also use DU, and USDA uses a automated system called GUS. GUS stands for the Guaranteed Underwriting System.

If you get an Automated Approval, loan officers will use this for your pre-approval. If you have a bad credit history, high debt to income ratios, or lack of down payment, the AUS will sometimes refer the loan to a manual underwrite, which could result in a longer turn time for your loan pre-approval answer

∘ ARE THERE ANY SPECIAL PROGRAMS IN KENTUCKY THAT HELP WITH DOWN PAYMENT OR NO MONEY DOWN LOANS FOR KY FIRST TIME HOME BUYERS?

Answer: There are some programs available to KY First Time Home Buyers that offer zero down financing: KHC, USDA, VA, Fannie Mae Home Possible and HomePath, HUD $100 down and City and Welcome Grants are all available to Kentucky First Time Home buyers if you qualify for them.

∘ WHEN CAN I LOCK IN MY INTEREST RATE TO PROTECT IT FROM GOING UP WHEN I BUY MY FIRST HOME?

Answer: You typically can lock in your mortgage rate and protect it from going up once you have a home picked-out and under contract. You can usually lock in your mortgage rate for free for 90 days, and if you need more time, you can extend the lock in rate for a fee to the lender in case the home buying process is taking a longer time.

The longer the term you lock the rate in the future, the higher the costs because the lender is taking a risk on rates in the future.

Interest rates are kind of like gas prices, they change daily, and the general trend is that they have been going up since the Presidential election in November 2016.

∘ HOW MUCH MONEY DO I NEED TO PAY TO CLOSE THE LOAN?

Answer: Depending on which loan program you choose, the outlay to close the loan can vary. Typically you will need to budget for the following to buy a home: Good faith deposit, usually less than $500 which holds the home for you while you close the loan. You get this back at closing; Appraisal fee is required to be paid to lender before closing. Typical costs run around $500-$650 for an appraisal fee; home inspection fees.

Even though the lender’s programs don’t require a home inspection, a lot of buyers do get one done. The costs for a home inspection runs around $300-$400. Lastly, termite report. They are very cheap, usually $50 or less, and VA requires one on their loan programs. FHA, KHC, USDAS, Fannie Mae does not require a termite report, but most borrowers get one done.

There are also lender costs for title insurance, title exam, closing fee, and underwriting fees that will be incurred at closing too. You can negotiated the seller to pay for these fees in the contract, or sometimes the lender can pay for this with a lender credit. The lender has to issue a breakdown of the fees you will incur on your loan pre-approval.

HOW LONG IS MY PRE-APPROVAL GOOD FOR ON A KENTUCKY MORTGAGE LOAN?

Answer: Most lenders will honor your loan pre-approval for 60 days. After that, they will have to re-run your credit report and ask for updated pay stubs, bank statements, to make sure your credit quality and income and assets has not changed from the initial loan pre-approval.

HOW MUCH MONEY DO I HAVE TO MAKE TO QUALIFY FOR A MORTGAGE LOAN IN KENTUCKY?

Answer: The general rule for most FHA, VA, KHC, USDA and Fannie MAe loans is that we run your loan application through the Automated Underwriting systems, and it will tell us your max loan qualifying ratios.

There are two ratios that matter when you qualify for a mortgage loan. The front-end ratio, is the new house payment divided by your gross monthly income. The back-end ratio, is the new house payment added to your current monthly bills on the credit report, to include child support obligations and 401k loans.

Car insurance, cell phone bills, utilities bills does not factor into your qualifying rations.

If the loan gets a refer on the initial desktop underwriting findings, then most programs will default to a front end ratio of 31% and a back-end ratio of 43% for most government agency loans that get a refer. You then take the lowest payment to qualify based on the front-end and back-end ratio.

So for example, let’s say you make $3000 a month and you have $400 in monthly bills you pay on the credit report. What would be your maximum qualifying house payment for a new loan?

Take the $3000 x .43%= $1290 maximum back-end ratio house payment. So take the $1290-$400= $890 max house payment you qualify for on the back-end ratio.

Then take the $3000 x .31%=$930 maximum qualifying house payment on front-end ratio.

So now your know! The max house payment you would qualify would be the $890, because it is the lowest payment of the two ratios.

Kentucky Welcome Home Grant 2024 Income Limits for the $20,000 Grant.

see below:👇 hit link for Welcome Home Grants Program 2024

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).