A Kentucky Mortgage Loan Officer that has closed over 600 home loans specializing in Kentucky First Time Homebuyer Loans to include the following FHA, VA, USDA, Rural Housing, Down Payment Assistance Loan from Kentucky Housing Corp or KHC and the Fannie Mae Home Path HUD $100 Down Mortgage Program in Kentucky. Call/Text 502-905-3708 with your mortgage questions or email kentuckyloan@gmail.com I try to respond to all requests within minutes during regular business hours. NMLS# 57916 Joel Lobb Loan Originator, American Mortgage Solutions NMLS ID. 1364 Equal Housing Lender

Are you a first-time homebuyer in Kentucky looking to navigate the world of home loans? Understanding the various types of home loan programs available to you can help you make informed decisions about financing your dream home. In this article, we’ll explore different home loan programs, including their credit score requirements, down payment requirements, bankruptcy considerations, debt-to-income ratio requirements, loan limits, and income limits.

Kentucky FHA Loans

Kentucky FHA Credit Score Requirements:

Minimum credit score typically ranges from 500 to 580, depending on the lender.

Kentucky FHA Down Payment Requirements:

A down payment as low as 3.5% of the purchase price is required. 10% down payment required for scores below 580

Kentucky FHA Bankruptcy Requirements:

Chapter 7 bankruptcy: Generally, two years must have passed since the discharge date.

Chapter 13 bankruptcy: Typically, one year of on-time payments and approval from the bankruptcy court are required.

Kentucky FHA Debt-to-Income Ratio Requirements:

Front-end ratio (housing expenses): Up to 31% of gross monthly income.

Back-end ratio (total monthly debt payments): Up to 43% of gross monthly income.

Up to 45% and 56% respectively for borrowers with higher credit scores, down payment and reserves along with good residual income

Kentucky FHA Loan Limits and Income Limits:

Loan limits vary by county and property type. Currently $498,257 in all Kentucky Counties

Income limits—-No income limits just loan limits.

Kentucky VA Loans

Kentucky VA Credit Score Requirements:

While there is no official minimum credit score requirement, most lenders prefer a score of 580 to 620 or higher.

Kentucky VA Down Payment Requirements:

No down payment is required for eligible veterans, active-duty service members, and certain spouses.

Kentucky VA Bankruptcy Requirements:

Chapter 7 bankruptcy: Generally, two years must have passed since the discharge date.

Chapter 13 bankruptcy: Typically, one year of on-time payments and approval from the bankruptcy court are required.

Kentucky VA Debt-to-Income Ratio Requirements:

Flexible debt-to-income ratio requirements, with consideration given to residual income.

Kentucky VA Loan Limits and Income Limits:

VA loan limits do not apply, but lenders may have their own limits.

No specific income limits, but income must be sufficient to cover monthly expenses.

Kentucky USDA Loans

Kentucky USDA Credit Score Requirements:

No minimum score, but credit score typically ranges from 580 and above, depending on the lender.

Kentucky USDA Down Payment Requirements:

No down payment is required for eligible properties in designated rural areas.

Kentucky USDA Bankruptcy Requirements:

Chapter 7 bankruptcy: Generally, three years must have passed since the discharge date.

Chapter 13 bankruptcy: Typically, one year of on-time payments and approval from the bankruptcy court are required.

Kentucky USDA Debt-to-Income Ratio Requirements:

Maximum total debt-to-income ratio is usually 45%.

Kentucky USDA Loan Limits and Income Limits:

Loan limits vary by county.

Income limits are based on area median income and household size.

Kentucky Conventional Loans

Kentucky Conventional Credit Score Requirements:

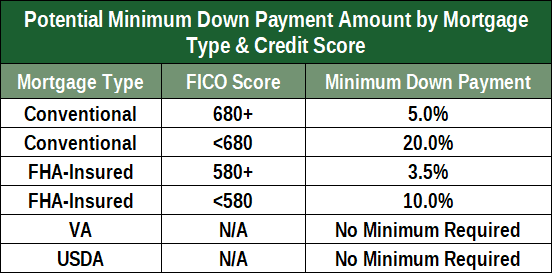

Minimum credit score typically ranges from 620 to 680, depending on the lender and loan type.

Kentucky Conventional Down Payment Requirements:

Down payment requirements can range from 3% to 20% or more, depending on the loan type and borrower qualifications.

Kentucky Conventional Bankruptcy Requirements:

Chapter 7 bankruptcy: Generally, four years must have passed since the discharge date.

Chapter 13 bankruptcy: Typically, two years of on-time payments and approval from the bankruptcy court are required.

Debt-to-Income Ratio Requirements:

Maximum total debt-to-income ratio is typically 43% to 50%, depending on the loan type and borrower qualifications.

Loan Limits and Income Limits:

Loan limits vary by property type and location.

No specific income limits, but income must be sufficient to qualify for the loan amount.

Conclusion

As a first-time homebuyer in Kentucky, you have several home loan programs to choose from, each with its own requirements and benefits. Whether you opt for an FHA loan, VA loan, USDA loan, or conventional loan, it’s essential to understand the credit score requirements, down payment requirements, bankruptcy considerations, debt-to-income ratio requirements, loan limits, and income limits associated with each program. Working with a knowledgeable lender can help you navigate the process and find the best loan program for your financial situation and homeownership goals.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

What is the minimum credit score I need to qualify for a Kentucky mortgage currently?

Question:

What is the current minimum credit scores needed to qualify for a Kentucky mortgage Loan?

Answer:

The minimum credit score needed to qualify for a Kentucky mortgage depends on the type of loan program you are looking to obtain, this could be the reason that you have received conflicting answers.

The most common types of mortgage are Conventional, FHA, USDA, VA, and KHC mortgage loans in Kentucky. I’ll explain each briefly below and the minimum credit score needed to qualify for each loan program. Keep in mind these are continuously changing and can vary by lender do to credit overlays.

Kentucky Conventional or Fannie Mae

Conventional loans make up the majority of mortgages in the US. They are also known as conforming loans, because they conform to specific guidelines set by Fannie Mae and Freddie Mac.

Minimum Credit Score is 620

What Are the Conforming Loan Limits for 2024?

Property Type Minimum Conforming Loan Limit Maximum Conforming Loan Limit

One-unit $766,550 $1,149,825

Two-unit $981,500 $1,472,250

Three-unit $1,186,350 $1,779,525

Four-unit $1,474,400 $2,211,600

You can use a conventional loan to buy a primary residence, second home, or rental property

Conventional loans are available in fixed rates, adjustable rates (ARMs), and offer many loan terms usually from 10 to 30 years

Down payments as low as 3% and 5% depending on Home Ready or straight conventional loan.

No monthly mortgage insurance with a down payment of at least 20%

Max Debt to Income Ratio of 50%

KENTUCKY FHA MORTGAGE

An FHA loan is a mortgage issued by federally qualified lenders and insured by the Federal Housing Administration (FHA). FHA loans are designed for low-to-moderate income borrowers who are unable to make a large down payment.

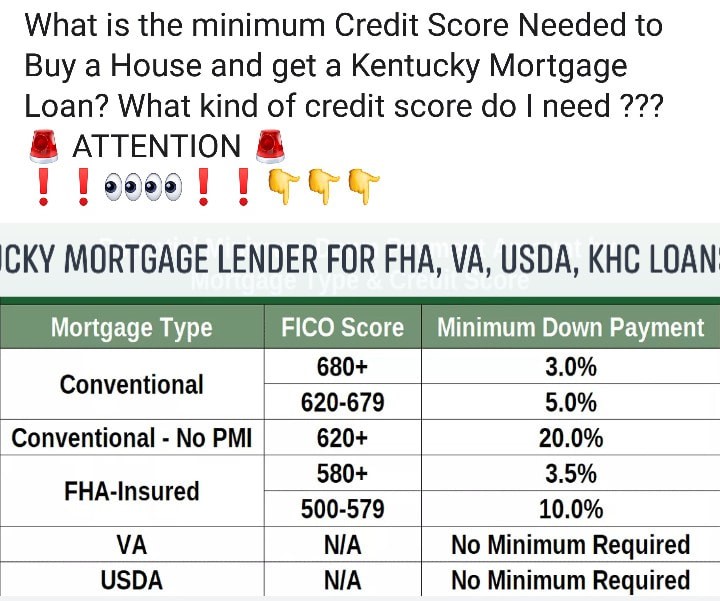

Minimum Credit Score is 500 with at least 10% down

Minimum Credit Score is 580 if you put less than 10% down

The maximum loan amount varies by Geographical Area, for 2024 is $498,257

Upfront and Monthly Mortgage Insurance is required regardless of the Loan to Value

FHA Loans are only available for financing primary residences

Maximum Debt to Income Ratio of 50% (unless mitigating factors justify allowing a higher DTI) up to 57% in some instances with strong compensating factors.

Primary Residents only (no rentals/investment properties)

Debt to income ratios no more than 45% with GUS approval and 29 and 41% with a manual underwrite.

Only Need a 580 Credit Score to Apply*** Most USDA loans need a 620 or score higher to get approved through their automated underwriting system called GUS. 640 usually required for an automated approval upfront.

No bankruptcies (Chapter 7) last 3 years and no foreclosure last 3 years. If Chapter 13 bankruptcy possible to go on after 1 year

KENTUCKY VA Mortgage

100% Financing Available up to qualifying income and entitlement

Must be eligible veteran with Certificate of Eligibility. We can help get this for veterans or active duty personnel.

No Down Payment Required

Seller Can Pay ALL Your Closing Costs

No Monthly Mortgage Insurance

Minimum 580 typically Credit Score to Apply–VA does not have a minimum credit score but lenders will create credit overlays to protect their interest.

Active Duty, Reserves, National Guard, & Retired Veterans Can Apply

No bankruptcies or foreclosures in last 2 years and a clear CAVIRS

Debt to income ratios vary, but usually 55% back-end ratio with a fico score over 620 will get it done on qualifying income and if it is a manual underwrite, 29% and 41% respectively

Can use your VA loan guaranty more than once, and in some cases, can have two existing VA loans out at they same time. Call or email for more info on this scenario.

Cost of VA loan appraisal in Kentucky now costs a minimum $605 with a termite report needed on all purchase and refinance transactions unless a condo.

2 year work history needed on VA loans unless you can show a legitimate excuse, ie. off work due to injury, schooling, education etc.

You cannot use your GI Bill for income qualifying for the mortgage payment.

KENTUCKY HOUSING DOWN PAYMENT ASSISTANCE 100 FINANCING

Down Payment: There are still housing programs that exist for Kentucky home buyers whereas you can purchase a home with no down payment. You will need a 620 mid credit score to purchase a home using the KHC loan programs for their no down payment credit requirements.

How the Down Payment Assistance Program (DAP) Works

Down payment assistance loans are available up to $10,000 and is paid back over a period of ten years at a current rate of 3.75%.

Assistance in the form of a loan up to $10,000 in $100 increments.

Repayable over a 10-year term at 3.75 percent.

Available to all KHC first-mortgage loan recipients

If you have questions about qualifying as first time home buyer in Kentucky, please call, text, email or fill out free prequalification below for your next mortgage loan pre-approval.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people

What credit score do you need for a Kentucky mortgage loan approval in 2024

There’s no universal minimum credit score needed for a mortgage, but a better credit score will give you more options. (iStock)

If you’re trying to get a mortgage, your credit score matters. Mortgage lenders use credit scores — as well as other information — to assess your likelihood of repaying a loan on time.

Because credit scores are so important, lenders set minimum scores you must have in order to qualify for a mortgage with them. Minimum credit score varies by lender and mortgage type, but generally, a higher score means better loan terms for you.

Let’s look at which loan types are best for different credit scores.

Credit score needed to buy a house

Mortgage lending is risky, and lenders want a way to quantify that risk. They use your three-digit credit score to gauge the risk of loaning you money since your credit score helps predict your likelihood of paying back a loan on time. Lenders also consider other data, such as your income, employment, debts and assets to decide whether to offer you a loan.

Different lenders and loan types have different borrower requirements, loan terms and minimum credit scores. Here are the requirements for some of the most common types of mortgages.

Conventional loan

Minimum credit score: 620

A conventional loan is a mortgage that isn’t backed by a federal agency. Most mortgage lenders offer conventional loans, and many lenders sell these loans to Fannie Mae or Freddie Mac — two government-sponsored enterprises. Conventional loans can have either fixed or adjustable rates, and terms ranging from 10 to 30 years.

You can get a conventional loan with a down payment as low as 3% of the home’s purchase price, so this type of loan makes sense if you don’t have enough for a traditional down payment. However, if your down payment is less than 20%, you’re required to pay for private mortgage insurance (PMI), which is an insurance policy designed to protect the lender if you stop making payments. You can ask your servicer to cancel PMI once the principal balance of your mortgage falls below 80% of the original value of your home.

FHA loan

Minimum credit score (10% down): 500

Minimum credit score (3.5% down): 580

FHA loans are backed by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). The FHA incentivizes lenders to make mortgage loans available to borrowers who might not otherwise qualify by guaranteeing the federal government will repay the mortgage if the borrower stops making payments. This makes an FHA loan a good option if you have a lower credit score.

FHA loans come in 15- or 30-year terms with fixed interest rates. Unlike conventional mortgages, which only require PMI for borrowers with less than 20% down, all FHA borrowers must pay an up-front mortgage insurance premium (MIP) and an annual MIP, as long as the loan is outstanding.

VA loan

Minimum credit score: N/A

VA loans are mortgages backed by the U.S. Department of Veterans Affairs (VA). The VA guarantees loans made by VA-approved lenders to qualifying veterans or service members of the U.S. armed forces, or their spouses. This type of loan is a great option for veterans and their spouses, especially if they don’t have the best credit and don’t have enough for a down payment.

VA loans are fixed-rate mortgages with 10-, 15-, 20- or 30-year terms.

Most VA loans don’t require a down payment or monthly mortgage insurance premiums. However, they do require a one-time VA funding fee, that ranges from 1.4% to 3.6% of the loan amount.

USDA loan

Minimum credit score: N/A

The U.S. Department of Agriculture guarantees loans for borrowers interested in buying homes in certain rural areas. USDA loans don’t require a minimum down payment, but you have to meet the USDA’s income eligibility limits, which vary by location.

All USDA mortgages have fixed interest rates and 30-year repayment terms.

USDA-approved lenders must pay an up-front guarantee fee of up to 3.5% of the purchase price to the USDA. That fee can be passed on to borrowers and financed into the home loan. If the home you want to buy is within an eligible rural area (defined by the USDA) and you meet the other requirements, this could be a great loan option for you.

What else do mortgage lenders consider?

Your credit score isn’t the only factor lenders consider when reviewing your loan application. Here are some of the other factors lenders use when deciding whether to give you a mortgage.

Debt-to-income ratio — Your debt-to-income (DTI) ratio is the amount of debt payments you make each month (including your mortgage payments) relative to your gross monthly income. For example, if your mortgage payments, car loan and credit card payments add up to $1,800 per month and you have a $6,000 monthly income, your debt-to-income ratio would be $1,800/$6,000, or 30%. Most conventional mortgages require a DTI ratio no greater than 36%. However, you may be approved with a DTI up to 45% if you meet other requirements.

Employment history — When you apply for a mortgage, lenders will ask for proof of employment — typically two years’ worth of W-2s and tax returns, as well as your two most recent pay stubs. Lenders prefer to work with people who have stable employment and consistent income.

Down payment — Putting money down to buy a home gives you immediate equity in the home and helps to ensure the lender recoups their loss if you stop making payments and they need to foreclose on the home. Most loans — other than VA and USDA loans — require a down payment of at least 3%, although a higher down payment could help you qualify for a lower interest rate or make up for other less-than-ideal aspects of your mortgage application.

The home’s value and condition — Lenders want to ensure the home collateralizing the loan is in good condition and worth what you’re paying for it. Typically, they’ll require an appraisal to determine the home’s value and may also require a home inspection to ensure there aren’t any unknown issues with the property.

How is your credit score calculated?

Most talk of credit scores makes it sound as if you have only one score. In fact, you have several credit scores, and they may be used by different lenders and for different purposes.

The three national credit bureaus — Experian, Equifax and TransUnion — collect information from banks, credit unions, lenders and public records to formulate your credit score. The most common and well-known scoring model is the FICO Score, which is based on the following five factors:

Payment history (35%) — A history of late payments will drag your score down, as will negative information from bankruptcies, foreclosures, repossessions or accounts referred to collections.

How much you owe (30%) — Your credit utilization ratio is the amount of revolving credit you’re using compared to your total available credit. For example, if you have one credit card with a $2,000 balance and a $4,000 credit limit, your credit utilization ratio is 50%. Credit scoring models view using a larger percentage of your available credit as risky behavior, so high balances and maxed-out credit cards will negatively impact your score.

Length of credit history (15%) — This factor considers the age of your oldest account, newest account and the average age of all your credit accounts. In general, the longer you’ve been using credit responsibly, the higher your score will be.

Types of accounts (10%) — Credit scoring models favor people who use a mix of credit cards, installment loans, mortgages and other types of credit.

Recent credit history (10%) — Lenders view applying for and opening several new credit accounts within a short period as a sign of financial trouble and it’ll negatively impact your score.

Ready to shop around for a mortgage?If you want a personalized answer for your unique situation call, text, or email me or visit my website below:

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

CONFIDENTIALITY NOTICE: This message is covered by the Electronic Communications Privacy Act, Title 18, United States Code, §§ 2510-2521. This e-mail and any attached files are deemed privileged and confidential, and are intended solely for the use of the individual(s) or entity to whom this e-mail is addressed. If you are not one of the named recipient(s) or believe that you have received this message in error, please delete this e-mail and any attached files from all locations in your computer, server, network, etc., and notify the sender IMMEDIATELY at 502-327-9770. Any other use, re-creation, dissemination, forwarding, or copying of this e-mail and any attached files is strictly prohibited and may be unlawful. Receipt by anyone other than the named recipient(s) is not a waiver of any attorney-client, work product, or other applicable privilege. E-mail is an informal method of communication and is subject to possible data corruption, either accidentally or intentionally. Therefore, it is normally inappropriate to rely on legal advice contained in an e-mail without obtaining further confirmation of said advice.

There are 4 basic things that a Kentucky-First Time Homebuyers in 2024 needs to show a lender in order to get approved for a mortgage. Each category has so many what-ifs and sub plots that each box can read as its own novel. In other words, each category has so many variables that can affect what it takes to get approved, but without further adieu here are the four categories in no particular order as each without any of these items, you’re pretty much dead in the water:

1. Income

You need income. You need to be able to afford the home. But what is acceptable income? Let’s just say that there are two ratios mortgage underwriters look at to qualify you for mortgage payment:

First Ratio – The first ratio, top ratio or housing ratio. Basically, that means out of all the gross monthly income you make, that no more that X percent of it can go to your housing payment. The housing payment consists of Principle, Interest, Taxes, and Insurance. Whether you escrow or not every one of these items is factored into your ratio. There are a lot of exceptions to how high you can go, but let’s just say that if your ratio is 33% or less, generally, across the board, you’re safe.

Second Ratio- The second ratio, bottom ratio or debt ratio includes the housing payment, but also adds all of the monthly debts that the borrower has. So, it includes housing payment as well as every other debt that a borrower may have. This would include, Auto loans, credit cards, student loans, personal loans, child support, alimony….basically any consistent outgoing debt that you’re paying on. Again, if you’re paying less than 45% of your gross monthly income to all of the debts, plus your proposed housing payment, then……generally, you’re safe. You can go a lot higher in this area, but there are a lot of caveats when increasing your back ratio.

What qualifies as income? Basically, it’s income that has at least a proven, two-year history of being received and pretty high assurances that the income is likely to continue for at least three years. What’s not acceptable? Unverifiable cash income, short term income and income that’s not likely to continue like unemployment income, student loan aid, VA education benefits, or short term disability are not allowed for a mortgage loan.

2. Assets

What the mortgage underwriter is looking for here is how much can you put down and secondly, how much will you have in reserves after the loan is made to help offset any financial emergencies in the future.

Do you have enough assets to put the money forth to qualify for the down payment that the particular program asks for? The only 100% financing or no money down loans still available in Kentucky for home buyers are available through USDA, VA, and KHC or Kentucky Housing Loans. Most other home buyers that don’t qualify for the no money down home loans mentioned above, will turn to the FHA program. FHA loans currently require a 3.5% down payment.

Kentucky Home buyers that have access to putting down at least 5% or more, will usually turn to Fannie Mae or Freddie Mac mortgage programs so they can get better pricing when it comes to mortgage insurance.

These assets need to be validated through bank accounts, 401k or retirements account and sometimes gifts from relatives or employer… Can you borrow the down payment? Sometimes. Generally, if you’re borrowing a secured loan against a secured asset you can use that. But rarely can cash be used as an asset. FHA will allow for gifts from relatives for down payments with little as 3.5% down but Fannie Mae will require a 20% down payment when a gift is being used for the down payment on the home.

The down payment scenarios listed above are for Kentucky Primary Residences only. There are stricter down payment requirements for investment homes made in Kentucky. 3. Credit

The minimum credit score is 500 for Kentucky FHA loans. However please keep in mind these two things: 1. Lenders credit their own overlays to increase the credit score threshold, most being 580 to 620, and secondly, if your credit score is below 580, you would need 10% minimum down payment, and if the credit score is over 580, then you can go with the minimum 3.5% down payment.

Obviously, if you have a higher credit score, this will increase your chances of getting approved for a Kentucky FHA Mortgage and possibly better rates and closing costs options.

Kentucky VA Mortgage loans requirements :

VA does not have a minimum credit score requirement, but if the credit score is below 620 few lenders will do the loan, but I am set up with several Kentucky VA lenders where I have closed them down to a 580 credit score, but the borrower had good compensating factors such as large down payment, low dti ratios, good job history and good residual income with no previous bankruptcies or foreclosures.

I would suggest if your credit scores are below 580, I would suggest on working on getting the scores up before you applied for a VA mortgage loan.

A lot of lenders will do a rapid rescore which in some cases can increase your credit scores in as little as 7-10 working days.

The federal Department of Veterans Affairs (VA) guarantees loans for current and former members of the military and their families. VA loans provide very favorable terms to eligible borrowers and have limited qualifying requirements. You can get a VA loan with no down payment so long as the home isn’t worth more than you pay for it, and there’s no minimum credit score to qualify. You also don’t have to pay for mortgage insurance, although you do have to pay an up-front funding fee of between .5% and 3.3% of the loan amount unless you fall within an exception for disabled vets or military widows or widowers.

Kentucky USDA Mortgage credit score requirements:

According to their guidelines, USDA will go down to a 580 credit score, but most lenders will want a 640 credit score. USDA uses an online system to underwrite the risk of the loan, and scores under 640 are very difficult to get approved.

Validating the Credit Score. Two or more eligible trade lines are necessary to validate an applicant’s credit report score. Eligible trade lines consist of credit accounts (revolving, installment etc.) with at least 12 months of repayment history reported on the credit report. At least one applicant whose income or assets are used for qualification must have a valid credit report score

The Rural Housing Service (RHS) operates under the federal Department of Agriculture to guarantee loans for rural home-buyers with limited income who can’t obtain conventional financing. The upside is that Kentucky USDA loans require no down payment. The downside is that they charge a steep up-front fee of 1% of the loan amount (which can be paid off over the entire loan term) and an annual fee of 0.35%.

Kentucky Fannie Mae and Freddie Mac Conventional Credit Score Requirements

These are considered “conventional loans’ that can be often be obtained with a 3% to 5% down payment. Of course, there are higher standards for conventional home financing.

The most common minimum credit score requirement to get approved today is a 620 FICO. This type of score is typical for people that have high credit card balances or a few delinquent payments in their past. The general consensus on Freddie Mac and Fannie Mae loans in Kentucky is that a 620 score is the entry-point to qualify, but you will need thorough documentation of income with credit scores in the 620 to 640 range.

You will have a better shot to be approved for a mortgage-backed by Fannie or Freddie with a 680-credit score and less strenuous underwriting.

Competitive Mortgage Rates and Fees

Monthly Mortgage Insurance Is Not Always Required

Ideal for First Time Home Buyers with Good Credit

As far as previous Bankruptcies and foreclosures:

Kentucky FHA Mortgage Loans currently requires 3 years removal from a foreclosure or short sale and 2 years on a bankruptcy with good re-established credit.

Kentucky Fannie Mae Mortgage Loans currently requires 4 years removal from bankruptcy, and 7 years on a foreclosure.

Kentucky VA Mortgage Loans currently requires 2 years of removal from bankruptcy or foreclosure with good re established credit.

Kentucky USDA loans require 3 years of removal from bankruptcy and foreclosure with good reestablished credit.

4. Appraisal

Generally, there’s nothing you can do to affect this. The bottom line here is…..” is the value of the house at least the value of what you’re paying for it?” If not, then not good things start to happen. Generally, you’ll find fewer issues with values on purchase transactions, because, in theory, the realtor has done an accurate job of valuing the house prior to taking the listing. The big issue comes in refinancing. In purchase transactions, the value is determined as the

Lower of the value or the contract price!!!

That means that if you buy a $1,000,000 home for $100,000, the value is established at $100,000. Conversely, if you buy a $200,000 home and the value comes in at $180,000 during the appraisal, then the value is established at $180,000. Big issues….Talk to your loan officer.

For each one of these boxes, there are over 1,000 things that can affect if a borrower has reached the threshold to complete that box. So..talk to a great loan officer. There are so many loan officers that don’t know what they’re doing. But, conversely, there’s a lot of great ones as well. Your loan is so important! Get a great lender so that you know, for sure, that the loan you want, can be closed on!

Most lenders want a 580 to 620 credit score nowadays with no bankruptcies in the last 2 years and no foreclosures in the last 3 years. You have three fico scores from Experian, Equifax and Transunion credit reporting agencies and the lenders will throw out the high and low score and take the middle score of the borrower(s).

Credit scores range from 334 to 850, the higher the score the better. The Fico Versions used for mortgage credit scores are Version, 2,4 and 5 models for Experian, Equifax and Transunion. They’re a lot of different scoring models out there and I can walk you through that once I pull your credit.

For example if you have a 598, 625, 604 on each of the main three reporting agencies, then your qualifying fico score would be 604.

They always take the lowest middle score of both borrowers, so keep that in mind too if there is a co-borrower. So if your mid score is 616, and your co-borrower is 638, and we used both of your incomes, then the score used to qualify would be the 616 score.

Once I get the credit report, I can analyze your scores, If the scores are okay, then we can proceed with pre-approval. If we need to work on them, I can help do that too.

If you’re trying to get a mortgage, your credit score matters. Mortgage lenders use credit scores — as well as other information — to assess your likelihood of repaying a loan on time.

Because credit scores are so important, lenders set minimum scores you must have in order to qualify for a mortgage with them. Minimum credit score varies by lender and mortgage type, but generally, a higher score means better loan terms for you.

Let’s look at which loan types are best for different credit scores.

Credit score needed to buy a house

Mortgage lending is risky, and lenders want a way to quantify that risk. They use your three-digit credit score to gauge the risk of loaning you money since your credit score helps predict your likelihood of paying back a loan on time. Lenders also consider other data, such as your income, employment, debts and assets to decide whether to offer you a loan.

Different lenders and loan types have different borrower requirements, loan terms and minimum credit scores. Here are the requirements for some of the most common types of mortgages.

Conventional loan

Minimum credit score: 620

A conventional loan is a mortgage that isn’t backed by a federal agency. Most mortgage lenders offer conventional loans, and many lenders sell these loans to Fannie Mae or Freddie Mac — two government-sponsored enterprises. Conventional loans can have either fixed or adjustable rates, and terms ranging from 10 to 30 years.

You can get a conventional loan with a down payment as low as 3% of the home’s purchase price, so this type of loan makes sense if you don’t have enough for a traditional down payment. However, if your down payment is less than 20%, you’re required to pay for private mortgage insurance (PMI), which is an insurance policy designed to protect the lender if you stop making payments. You can ask your servicer to cancel PMI once the principal balance of your mortgage falls below 80% of the original value of your home.

FHA loan

Minimum credit score (10% down): 500

Minimum credit score (3.5% down): 580

FHA loans are backed by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). The FHA incentivizes lenders to make mortgage loans available to borrowers who might not otherwise qualify by guaranteeing the federal government will repay the mortgage if the borrower stops making payments. This makes an FHA loan a good option if you have a lower credit score.

FHA loans come in 15- or 30-year terms with fixed interest rates. Unlike conventional mortgages, which only require PMI for borrowers with less than 20% down, all FHA borrowers must pay an up-front mortgage insurance premium (MIP) and an annual MIP, as long as the loan is outstanding.

VA loan

Minimum credit score: N/A

VA loans are mortgages backed by the U.S. Department of Veterans Affairs (VA). The VA guarantees loans made by VA-approved lenders to qualifying veterans or service members of the U.S. armed forces, or their spouses. This type of loan is a great option for veterans and their spouses, especially if they don’t have the best credit and don’t have enough for a down payment.

VA loans are fixed-rate mortgages with 10-, 15-, 20- or 30-year terms.

Most VA loans don’t require a down payment or monthly mortgage insurance premiums. However, they do require a one-time VA funding fee, that ranges from 1.4% to 3.6% of the loan amount.

USDA loan

Minimum credit score: N/A

The U.S. Department of Agriculture guarantees loans for borrowers interested in buying homes in certain rural areas. USDA loans don’t require a minimum down payment, but you have to meet the USDA’s income eligibility limits, which vary by location.

All USDA mortgages have fixed interest rates and 30-year repayment terms.

USDA-approved lenders must pay an up-front guarantee fee of up to 3.5% of the purchase price to the USDA. That fee can be passed on to borrowers and financed into the home loan. If the home you want to buy is within an eligible rural area (defined by the USDA) and you meet the other requirements, this could be a great loan option for you.

What else do mortgage lenders consider?

Your credit score isn’t the only factor lenders consider when reviewing your loan application. Here are some of the other factors lenders use when deciding whether to give you a mortgage.

Debt-to-income ratio — Your debt-to-income (DTI) ratio is the amount of debt payments you make each month (including your mortgage payments) relative to your gross monthly income. For example, if your mortgage payments, car loan and credit card payments add up to $1,800 per month and you have a $6,000 monthly income, your debt-to-income ratio would be $1,800/$6,000, or 30%. Most conventional mortgages require a DTI ratio no greater than 36%. However, you may be approved with a DTI up to 45% if you meet other requirements.

Employment history — When you apply for a mortgage, lenders will ask for proof of employment — typically two years’ worth of W-2s and tax returns, as well as your two most recent pay stubs. Lenders prefer to work with people who have stable employment and consistent income.

Down payment — Putting money down to buy a home gives you immediate equity in the home and helps to ensure the lender recoups their loss if you stop making payments and they need to foreclose on the home. Most loans — other than VA and USDA loans — require a down payment of at least 3%, although a higher down payment could help you qualify for a lower interest rate or make up for other less-than-ideal aspects of your mortgage application.

The home’s value and condition — Lenders want to ensure the home collateralizing the loan is in good condition and worth what you’re paying for it. Typically, they’ll require an appraisal to determine the home’s value and may also require a home inspection to ensure there aren’t any unknown issues with the property.

How is your credit score calculated?

Most talk of credit scores makes it sound as if you have only one score. In fact, you have several credit scores, and they may be used by different lenders and for different purposes.

The three national credit bureaus — Experian, Equifax and TransUnion — collect information from banks, credit unions, lenders and public records to formulate your credit score. The most common and well-known scoring model is the FICO Score, which is based on the following five factors:

Payment history (35%) — A history of late payments will drag your score down, as will negative information from bankruptcies, foreclosures, repossessions or accounts referred to collections.

How much you owe (30%) — Your credit utilization ratio is the amount of revolving credit you’re using compared to your total available credit. For example, if you have one credit card with a $2,000 balance and a $4,000 credit limit, your credit utilization ratio is 50%. Credit scoring models view using a larger percentage of your available credit as risky behavior, so high balances and maxed-out credit cards will negatively impact your score.

Length of credit history (15%) — This factor considers the age of your oldest account, newest account and the average age of all your credit accounts. In general, the longer you’ve been using credit responsibly, the higher your score will be.

Types of accounts (10%) — Credit scoring models favor people who use a mix of credit cards, installment loans, mortgages and other types of credit.

Recent credit history (10%) — Lenders view applying for and opening several new credit accounts within a short period as a sign of financial trouble and it’ll negatively impact your score.

What Fico Score is Used for a Mortgage Loan Approval

Which Lenders Use Which FICO Scores?

With the exception of the mortgage market, which is heavily regulated, lenders can generally choose which FICO score they use when doing a credit check. However, they tend to use certain versions depending on the kind of credit for which you’re applying. Here’s a look at the most common FICO scores used for each type of credit.

Mortgages

When you’re taking out a mortgage, there’s a good chance that the loan will end up being bought by Fannie Mae or Freddie Mac. As with many other aspects of the housing market, these massive government-backed mortgage companies dictate which FICO scores can be used by home lenders. Here are the FICO scores used in credit reports generated by the three credit bureaus (as well as the alternative names the bureaus use to advertise them):9

Experian: FICO Score 2 (Experian/Fair Isaac Risk Model V2SM)

The reason mortgage lenders use older FICO Scores is because they don’t have a choice. They are essentially forced to use them.

Unlike every other industry, mortgage lenders don’t have the flexibility to choose the scoring model brand or generation they want to use. Mortgage lenders must follow the direction of the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as it pertains to scoring models.

The GSEs play an important role in mortgage lending. These publicly traded companies buy mortgages from banks, bundle them together, and sell them to investors. This frees up funds so that banks can offer new mortgages to additional homebuyers.

For a bank to sell a mortgage to Fannie Mae or Freddie Mac, the loan has to meet certain guidelines. Some of these guidelines require borrowers to have a minimum credit score under specific FICO Score generations.

If a lender uses a different scoring model other than what the GSEs approve when it underwrites a mortgage, it probably won’t be able to sell that mortgage after it issues the loan. This limits the lender’s ability to write new loans because it will have less money available to lend to future borrowers.

Ready to shop around for a mortgage?

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

CONFIDENTIALITY NOTICE: This message is covered by the Electronic Communications Privacy Act, Title 18, United States Code, §§ 2510-2521. This e-mail and any attached files are deemed privileged and confidential, and are intended solely for the use of the individual(s) or entity to whom this e-mail is addressed. If you are not one of the named recipient(s) or believe that you have received this message in error, please delete this e-mail and any attached files from all locations in your computer, server, network, etc., and notify the sender IMMEDIATELY at 502-327-9770. Any other use, re-creation, dissemination, forwarding, or copying of this e-mail and any attached files is strictly prohibited and may be unlawful. Receipt by anyone other than the named recipient(s) is not a waiver of any attorney-client, work product, or other applicable privilege. E-mail is an informal method of communication and is subject to possible data corruption, either accidentally or intentionally. Therefore, it is normally inappropriate to rely on legal advice contained in an e-mail without obtaining further confirmation of said advice.