Qualifications for a USDA Loan to Buy a Home in Kentucky

Qualifications for a USDA Loan to Buy a Home in Kentucky

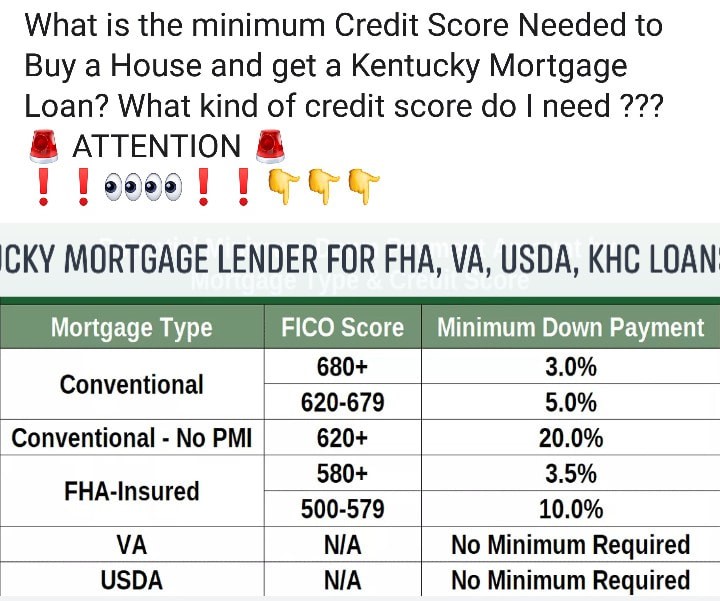

Kentucky First-Time Homebuyer Loan Programs for FHA, VA, KHC and USDA Mortgage Loans in Kentucky

A Kentucky Mortgage Loan Officer that has closed over 600 home loans specializing in Kentucky First Time Homebuyer Loans to include the following FHA, VA, USDA, Rural Housing, Down Payment Assistance Loan from Kentucky Housing Corp or KHC and the Fannie Mae Home Path HUD $100 Down Mortgage Program in Kentucky. Call/Text 502-905-3708 with your mortgage questions or email kentuckyloan@gmail.com I try to respond to all requests within minutes during regular business hours. NMLS# 57916 Joel Lobb Loan Originator, American Mortgage Solutions NMLS ID. 1364 Equal Housing Lender

Qualifications for a USDA Loan to Buy a Home in Kentucky

If you’re planning to buy a home in Kentucky in 2024, here are some essential steps to consider:

1. Focus on improving your credit score to qualify for a mortgage with a low interest rate.

2. Manage your debt-to-income ratio by repaying existing debt, increasing your income, or both.

3. Ensure timely payments on all accounts to maintain a good credit score.

4. Get pre-approved for a mortgage before searching for a home to know your affordability.

5. Keep credit card utilization below 30% and seek down payment assistance programs if needed.

Here are action steps you can take right now to buy a home in Kentucky in 2024

1. Focus on your credit score

FICO credit scores are among the most frequently used credit scores, and range from 350-800 (the higher, the better). A consumer with a credit score of 750 or higher is considered to have excellent credit, while a consumer with a credit score below 620 is considered to have poor credit.

To qualify for a mortgage and get a low mortgage rate, your credit score matters.

Each credit bureau collects information on your credit history and develops a credit score that lenders use to assess your riskiness as a borrower. If you find an error, you should report it to the credit bureau immediately so that it can be corrected.

2. Manage your debt-to-income ratio

Many lenders evaluate your debt-to-income ratio when making credit decisions, which could impact the interest rate you receive.

A debt-to-income ratio is your monthly debt payments as a percentage of your monthly income. Lenders focus on this ratio to determine whether you have enough excess cash to cover your living expenses plus your debt obligations.

Since a debt-to-income ratio has two components (debt and income), the best way to lower your debt-to-income ratio is to:

3. Pay attention to your payments

Simply put, lenders want to lend to financially responsible borrowers.

Your payment history is one of the largest components of your credit score. To ensure on-time payments, set up autopay for all your accounts so the funds are directly debited each month.

FICO scores are weighted more heavily by recent payments so your future matters more than your past.

In particular, make sure to:

4. Get pre-approved for a mortgage before you start shopping for a home loan.

Too many people find their home and then get a mortgage.

Switch it.

Get pre-approved with a lender first. Then, you’ll know how much home you can afford.

To get pre-approved, lenders will look at your income, assets, credit profile and employment, among other documents.

5. Keep credit utilization low on your credit cards

Lenders also evaluate your credit card utilization, or your monthly credit card spending as a percentage of your credit limit.

Ideally, your credit utilization should be less than 30%. If you can keep it less than 10%, even better.

For example, if you have a $10,000 credit limit on your credit card and spent $3,000 this month, your credit utilization is 30%.

Here are some ways to manage your credit card utilization:

6. Look for down payment assistance in Kentucky

There are various types of down payment assistance, even if you have student loans.

Here are a few:

There are federal, state and local assistance programs as well so be on the look out.

If you want a personalized answer for your unique situation call, text, or email me or visit my website below:

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

When shopping for a Kentucky mortgage loan, keep in mind that mortgage rates can change daily. Different lenders have varying fees, and they may sell your loan to another bank. Your middle credit score is crucial, and good credit leads to better rates. Knowing your Annual Percentage Rate (APR) and reducing closing costs are important. Finally, you can refinance your home loan anytime and get a mortgage loan after a foreclosure with certain waiting periods.

Just like the stock market, mortgage rates change throughout the day. Mortgage rates you see today may not be available tomorrow. If you are in the market for a mortgage loan, be sure to check the current rates being offered by lenders. If you have already done your research and have found your dream home consider locking in your rate as soon as possible.

2. Different Lenders Charge Different Fees

Don’t expect every lender to charge the same fees for a mortgage loan. Every lender structures their fees differently, which is why it is important to shop with at least 3 lenders to compare. Next time you apply for a mortgage loan pay attention to the rates, points being charged and closing costs.

3. Lenders Can Sell Your Loan to Another Bank

Many borrowers have experience getting a mortgage loan with a certain lender only to find out that the loan has been sold to another bank. This occurs because lenders need to free up their liabilities in order to make room to give out more loans. This does not affect your mortgage whatsoever, but it’s important to pay close attention to your mortgage statement and any correspondence you receive in the mail to make sure you do not make payments to the wrong bank.

4. Your Middle Credit Score Matters

When you apply for a mortgage loan, the lender will pull your credit scores from three credit bureaus (Transunion, Equifax and Experian) to help them determined if you are credit worthy. Your middle score of the three is what lenders will use for loan qualification. However, the underwriter will review all three scores as part of the loan underwriting process. If you pull your own credit score through a website online, the credit scores displayed to you may be different than what lenders use because they use different reporting systems.

5. You Can Refinance Your Home Loan Anytime

You can refinance your mortgage anytime, but it doesn’t necessarily mean you should. Think about why you want to refinance. Is because you want to lower your monthly payments, to change the type of loan you are in or to take cash out from your equity? Whatever the reason is, make sure that it makes financial sense.

6. You Can Get a Mortgage Loan After a Foreclosure

Many homeowners have experienced a foreclosure after the recent mortgage crisis. There is good news for these borrowers because they can get a mortgage loan after foreclosure. There are waiting periods involved, for example, to apply for an FHA loan you must wait three years after foreclosure to apply. If you want to get a conventional loan the waiting period is seven years from foreclosure. For those seeking a VA loan, the waiting period is two-years.

There are exceptions to the waiting periods, but you have to show the lender that your foreclosure was caused by an event outside your control, such as losing your job or being seriously ill.

8. Good Credit Allows you to Get Better Mortgage Rates

Good credit scores mean a better rate in any type of loan, especially a mortgage loan. Your credit heavily impacts the type mortgage loan you will qualify for. To maintain a good credit report, make sure you monitored it closely. One of the advantages to good credit is that more banks will want to compete for your business, therefore giving you leverage to negotiate the closing costs.

9. Know Your Annual Percentage Rate (APR)

Knowing your APR will allow you see the true cost of your loan. While the interest rate shows the annual cost of your loan, the APR includes other fees such as origination points, admin fees, loan processing fees, underwriting fees, documentation fees, private mortgage insurance and escrow fees.

There may be more or less fees included in the ARP from what we mentioned. To be sure what fees are included in the APR, ask your lender to give you a breakdown of the closing costs included.

10. You Can Always Reduce Closing Costs

One way to reduce closing costs is to have the sellers contribute towards the closing costs when purchasing your home. This can be negotiated between the buyer and the sellers in the purchase contract. The amount the seller can contribute will depend on the type of loan. Another way to save on closing costs is to have the lender give you a credit to cover out of pocket loan costs.

Joel Lobb

Mortgage Loan Officer

Individual NMLS ID #57916

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

https://kentuckyloan.blogspot.com

CONFIDENTIALITY NOTICE: This message is covered by the Electronic Communications Privacy Act, Title 18, United States Code, §§ 2510-2521. This e-mail and any attached files are deemed privileged and confidential, and are intended solely for the use of the individual(s) or entity to whom this e-mail is addressed. If you are not one of the named recipient(s) or believe that you have received this message in error, please delete this e-mail and any attached files from all locations in your computer, server, network, etc., and notify the sender IMMEDIATELY at 502-327-9770. Any other use, re-creation, dissemination, forwarding, or copying of this e-mail and any attached files is strictly prohibited and may be unlawful. Receipt by anyone other than the named recipient(s) is not a waiver of any attorney-client, work product, or other applicable privilege. E-mail is an informal method of communication and is subject to possible data corruption, either accidentally or intentionally. Therefore, it is normally inappropriate to rely on legal advice contained in an e-mail without obtaining further confirmation of said advice.

The difference in Kentucky USDA Direct loans vs. Kentucky USDA Guaranteed Loans

Down Payment: There are still housing programs that exist for Kentucky home buyers whereas you can purchase a home with no down payment. You will need a 620 mid credit score to purchase a home using the KHC loan programs for their no down payment credit requirements.

Down payment assistance loans are available up to $10,000 and is paid back over a period of ten years at a current rate of 3.75%.